A second opinion was delivered this week by Ron Sucik. He is a semi-retired expert with a long and distinguished career at TTX. I wrote a commentary about the TTX pool railcar business recently.

With his permission, here are a few key slides and market takeaways from Mr. Sucik.

The first market takeaway is an admission of a missed forecast he made last year and why. We anticipated a potential to capture motor carrier market share because of:

- Driver shortages

- Electronic logging device disruptions

- Fuel price increases

What we did not anticipate was:

- Precision scheduled railroading (PSR) adjustments

- Potential tariff implementation

Making a market outlook call and then adjusting to competitive moves by others (like trucking companies) doesn’t seem to be a competitive strength at many of the PSR rail headquarters.

There is a logical argument that suggests intermodal marketing seems primarily investor-centric.

Amidst the dynamic and deteriorating global market conditions of early 2020, supply-chain constituents that depend upon inland rail transport – like the international ports – are worried. What is the long-term game plan of their intermodal “partners?” The railroad messages to Wall Street are not relevant to these port partners.

A year ago, Sucik asked, “Where is the next layer of fruit?” Translation – what is the next growth segment for senior rail managers?

Here is a bold challenge as he asks, “Should the industry take a bold step backward and go after short-haul traffic, even if the margins aren’t as great?”

Oh my! One year later, and we are still waiting for a clear answer from a Class 1 railroad in regard to its attack plan for short-haul intermodal.

Perhaps the railroads have cut their costs too deeply. There is an argument that railroad operating departments may no longer have enough crews or locomotives necessary to pursue large new business volume initiatives. They have more track time space. But perhaps no reserve movable assets.

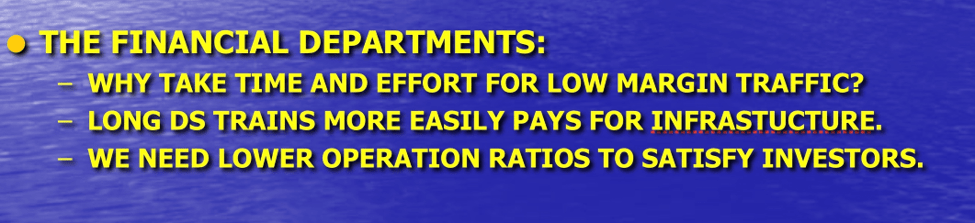

Railroad financial departments might instead believe, “Why take the time and effort for low-margin traffic. Long-distance service more easily pays for infrastructure, and we need a lower operating ratio to satisfy the investors.” That corporate attitude might be the inhibiting cultural factor, suggests Sucik.

Instead, it appears that the Class I railroads are sticking to a pricing scheme that targets the highest intermodal margin and cash flow. Collectively, they are not lowering prices to attract incremental customers. There appears to be a corporate fear that that action might lower their targeted quarterly margins.

Is this accurate? It appears so.

You the readers might disagree. If so, you should speak out and please present your logic.

With this as background, the alternate year 2020 volume forecast as seen by Ron Sucik is this. He predicts that “intermodal 2020 year-over-year volume will be flat.” That is not normal when we look at the past three or more decades of rail growth. There might be a possible recovery in the second half of the year helped by the year-over-year comparisons to the low numbers recorded during the second half of 2019.

Orders for new intermodal cars and containers, if any, will likely be very small in 2020.

There is a significant excess of railcars in the intermodal fleet. That excess has to be worked off either through railcar retirement or by business growth. Potential intermodal volume continues early in 2020 to remain with or shift to trucking.

As long as trucking has capacity and drivers – plus lower fuel prices – the railroads will face difficulty in capturing chunks of trucking’s market share.

Strategically, it is possible that as a consequence of trade policies some manufacturing activity might shift back to the United States. Yes, that would be good for the economy.

Ironically, that geographic shift might reduce intermodal rail market shifts, since long-haul movements of containers from ports to inland markets could be displaced by an increase in very short-haul inland trucking distribution changes – where intermodal has a smaller economic advantage.

Always looking for balance, what are other experts saying about intermodal? Who’s aggressive? I could not find a short-term aggressive spokesperson.

Sadly, it may be 2021 or possibly as late as 2022 for a turnaround in growth for intermodal – particularly if a recession should occur as a consequence of the global forces we are currently seeing. At this point that is a prudent reminder, and not a prediction.