Greetings!

SWARS is tomorrow (3/11 - I’ll be virtual, though it will be live: Southeast Association of Rail Shippers (swrailshippers.com) – my slides are attached, one is below); NEARS put out its multi-day virtual agenda (attached) for next month.

First, to the tweets:

- Rail Pulse – the alliance promoting visibility in carload freight, took a major step by hiring its phase one lead consultant, Princeton Consultants (a well-respected firm in the space despite its rather unfortunate name). R/P should prove to be a game-changer….

And from last week:

- Surprisingly, the just-released ’21 ASCE “Infrastructure Report Card” saw the US improve (from 2017), albeit slightly, from “D” to “C-“; with roads, transit, and dams, all receiving D's. Rails and ports – both having private investment -scored the highest, both receiving B's (I am confident that freight rail alone would have been B+).

- The eastern RR map is being redrawn, and the application to the STB by CSX to purchase the Pan Am may produce three winners: CSX gets the PAR and to St John (and likely approval); GWR gets the PAS and a bigger NE RR “cluster” and NS gets real IM access to NE (& GWR in the PAS).

Rail traffic is recovering from the Big Chill (as well as intermodal congestion) but the impacts on February are evident – many rails are beginning to reduce their just-reinstated guidance for Q1 volumes. Overall North American volumes grew 4% in January, and QTD stands at +1%; the hit in February – most of it concentrated in a single week (7), was total NA carloads -11% (4/20 commodities measured by the AAR’s RTI showed increases) and IM up 3% despite the cold. There were stories within the total, of course. Forest products are doing fine (up 6% US/C YTD) and so are autos (up 7% NA YTD despite the 22% drop last month).

- Oh, Mexico! – CL -30% (3/20) and IM -31%! The rebound has begun, but that’s a drop, all right.

- Oh, Texas – the US showed a 10% carload drop (4/20) – including Chems & Pete down ~14% - that’s CBR, of course (but easy comps) and no compensation from plastics when the world was frozen. IM, nonetheless, was up 5%.

- Used to winter up there: Canada showed only a 5% decline in carloads (9/20) and intermodal was up 18% (we’ll see when IANA data comes out but I am guessing some of that is further BC port market share gains).

- Intermodal remains the story; how long can it (“the never-ending peak” – JoC – of demand) re-stocking/consumer demand) keep up? In January, experts thought through Lunar New Year, but we’re well past that point. Maersk, which blew away earnings – and FY21 Guidance – expectations, thinks for the FY21 And what about the global supply chain issue (NYT, a bit late to the party: “Chaos strikes global shipping!”).

- Note – after taking some hits for service issues in the madcap rebound, it must be relaxing for rail IM managers, especially on the west coast, to see virtually no mention of rails service issues in the plethora of reports on shortages/congestion….

- And don’t buy the hype that the IM discount is going away – given the contract pricing lag, this will be good and improving business for a while yet….

- If perhaps not at the pace of week 9 (+19% - recovery – ice – on recovery – Covid)

- Encouraging that JBHunt has ordered some 6K containers; it is my opinion that the rails had a huge unforced error in 2018 when they didn’t have enough capacity to handle the spillover opportunity from the (regulatory-enhanced) record tight trucking market; the result is that much of the big rail IM growth of that year was in TOFC. That is of course the most fungible of all rail commodities and indeed, much of that business returned to the highway in the loose market conditions of 2019….

- Efforts continue to create a US manufacturer of containers – stay tuned….

- But also be thankful for the NA farmer – US/Canadian grain was up 19% (split 28/16, respectively); while we remember that “the investment road to ruin is paved with the boasts of commodity price bulls” (FT/Lex – which quoted one trader out of China: “Very few businesses could yield an almost guaranteed return as speculating on corn”). That said, the US grain bull market appears to be something that will last at a minimum through the 2021-22 crop year, according to:

- ADM, which thinks that recent USDA predictions are too conservative….

- The seasonal move from beans to corn is rail supportive (flows moving from a Gulf/PNW split – impacted by frozen rivers, of course - to the PNW); perhaps the remaining short-intermediate issue is whether farmers sit on expectations of even higher prices (and whether the freeze impacts input – ferts – prices and winter wheat production)

- It’s demand-driven – China/China/China, which imported 11mmt last year and despite efforts at self-sufficiency could get to 25mmt/year soon according to ADM) , and the return to political favor of ethanol.

- Notably big guidance forecasts from ADM, Deere, Bunge (“best environment in years for traders”).

- USDA planting estimates suggest the farmer is betting on the bull as estimates of planting acres go up sharply for corn and soybeans.

- Supercycle II of the 21st C?

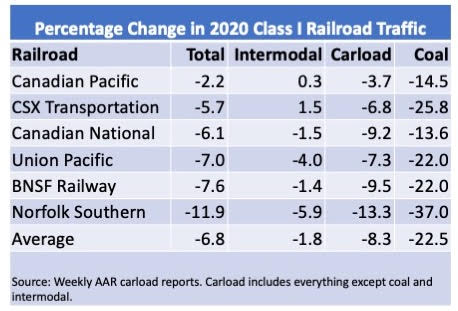

- Coal’s decline in the US of 12.5% for the month seems to be not so bad, relatively (but remember the “comps”); RTI reminds us that 2020 US coal revenues of $6.3B represent a 32% decline from the prior year and 61% from the 2011 peak. The EIA sees 2021 showing “expired tabby jump”, but as we have noted, while CSX seems to concur, NSC does not….

- Cars in storage remain about the same (24% of the total) despite the overall recovery (PSR, etc); meanwhile about a third of the NA high horsepower locos are also parked (PSR/longer, heavier trains, focus on loco productivity, and train starts/volume.