Greetings;

I will be a presenter at the free (!) virtual South East Association of Railroad Shippers spring conference (SEARS (tradewing.com) on Thursday; tomorrow I am joining the good folks at Commtrex (and, warning: Dick Kloster) for a webinar: CP+KSU – More, More, More! Just when I thought I was getting a chance to ponder industry fundamentals they (M&A) pull me back in….If the long period before the German invasion of France was known as the “Phony War”, this current period, ahead of one deadline Friday, might be called the “Letter War” – STB, DOJ, CP+KSU, and lots of letters pro & con. Let’s take a look….

- CP/KSU issued a press release stating their level of support had increased to 375 shippers – notably many intermodal (high-service) customers (XPO added).

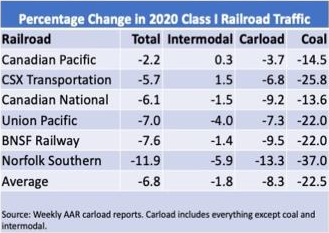

- Mea Culpa – not this time but I hear you all - I received a fair amount of pushback on my criticism of the arguments that PSR was, in effect bad for shippers. I had argued that PSR 1.0 was about cost-cutting, change & restructuring, but that 2.0 was the “pivot to growth”, citing the example of both Canadian carriers (I keep screaming in the dark “look to the North!”), and of CSX. One deep thinking rail insider wrote to me that “PSR is failing shippers. That’s simply a fact.” Despite his impeccable educational credentials, I humbly disagree….see CSX’s performance as it transitioned to PSR 2.0 (my label, not theirs) below; nope also CP.

- That said, CSX is currently having to severe service issues in the Alabama region, due to crew shortages, though not caused, as has often been the case, by furloughs and cost-cutting, but by scarcity of qualified applicants….

- Also concerning CSX, it is interesting to see their different tack compared to the other three of the US “Big 4”; with PAR still before the STB and facing (what is assumed to be manageable) opposition, they may feel that have enough on their plate in DC….Their outlook on that is to re-file on April 26 and close around year-end.

- The STB’s dance card is filling up – not just the PAR, the CP+KSU, the perhaps dormant CSXCN/Massena Lines, but now….the Watco purchase of the CN (WC) short lines in Wisconsin? This is a head-scratcher. Most of the issues raised are actually solved by a good short line, and Watco is surely that. In fact, this could be yet another sign, that for (more) good or (some) ill, Hunter lives! CN’s purchase of the WC under his tenure caused both a major improvement in service and a reduction in costs (for the railway, for the shipper) but also lingering hard feelings.

- The WSJ Heard on the Street came out in favor of the deal, sort of, but in favor of rails in general, waking up to the fact that since the fall of 2009 (before the Buffett purchase of BNSF), a basket of Rr stocks would have appreciated 862% versus the S&P 500 at ~300%. HoS then said this transaction could possibly unlock other deals (well….), but that rails – and these rails – would be valuable even without approval – finally, something either vaguely wrong or well-known….

- Comments to the STB closed yesterday (April 12) – with a decision on the comments and rebuttals and a review schedule expected between “about 10 days” to “2-3 weeks”.

- Remember that, despite it being repeatedly brought up in comments, the semi-proposed CP-NS deal is not comparable, and actually deserved a rejection (of the deal, and the VT); also CP’s position in 2001 on the KSU exemption is irrelevant. There is no one at CP then in a position of power now….

- Remember that, despite it being repeatedly brought up in comments, the semi-proposed CP-NS deal is not comparable, and actually deserved a rejection (of the deal, and the VT); also CP’s position in 2001 on the KSU exemption is irrelevant. There is no one at CP then in a position of power now….

- Included in the late comments was an objection to both the exemption and the Voting Trust by the Department of Justice. This was perceived to be a Very Big Deal, and perhaps we’ll find that it is, but the STB doesn’t work for the DoJ (rather, the DoT). Furthermore, the DoJ has seemingly objected to every merger since the Baltimore + Ohio (don’t google, I made that up). At least we know where DoJ has been focusing its anti-trust brainpower rather than on that emerging tech industry...I found their commentary to be….irksome.

- DoJ doesn’t (yet) have an opinion on the deal, but rather on the exemption and the VT.

- The DoJ is apparently unaware of that 1950s innovation, the Interstate Highway System.

- The DoJ cites the 2016 CP-NS proposal, rather than, say, the more relevant SFSP (or UPSP, or BNSF, or CRR, or….)

- They answer their own major, first objection – that VT would cause reduced competition between the companies (there is none), and that wouldn’t make sense in an end-to-end combination. The argument that “absent the trust” KSU shareholders would have an incentive to protect their own interests belies the impact of Dave Starling as Trustee and the fact that in an end-to-end, KSU pursuing its own interests helps itself and the proposed combination.

- They think that a VT even in an obviously end-to-end combination “makes a mockery of the (ST) Board’s authority” goes against successful history (again see SF-SP post rejection) and that a VT may prevent the Board from “effecting a successful divestiture” (again see SFSP) and

- Says remaining purchasers may be “entities without railroad experience”….but they are obviously looking at PE/Infra interest would retain existing management and simply change ownership/shareholders (many shareholders lack direct railroad experience).

- A spinoff is ridiculous in its own right but – unmentioned, an IPO wouldn’t be (KSU would retain the best growth potential in the industry)\

- The mentioned “less harmful” mechanisms that can achieve the same results as a VT (breakup fees, etc) actually don’t – they can offer some protection to the shareholder but not to the railway and its operations, themselves….

- CP+KSU responded:

- They “asserted their right to have the STB review their combination under a (the) waiver.”

- They made it clear that there is no deal without a VT – “there will not be a CP-KCS transaction” without it.

- They received an interesting endorsement from William Clyburn Jr, one of the three members of the STB in 2001 who said that regarding the KSU exemption “the reasons are just as valid today as they were” in 2001…

- They received perhaps an even more interesting endorsement from retired Senator Byron Dorgan of ND, a long time critic of the rails and self-described longtime “skeptic of railroad mergers” and a leading proponent of the 2001 moratorium/exemption (kudos to the CP Board for this letter); Dorgan writes that this is the one unique transaction among large US railroads, that is beneficial and that does not raise concerns related to east-West transcontinental railroad mergers”, and cites benefits to his former constituents in North Dakota. But Dorgan goes on to raise an issue that has caused me to rethink my view that the STB will “kick the can” and simply remove the exemption prior to ultimately approving the obviously pro-competitive deal:

- Echoing comments by a retired head of American Honda logistics, Dorgan remains concerned about further (Big 4/transcon) consolidation in the industry (as do I), and noted that the new merger rules of 2001 have “held back the tide of harmful transcon mergers” for two decades (I would say that have helped hold back the tide….). He then goes on to write “I urge the Board not to crack that dam by applying these

(“new”) rules to the CP-KCS proposal which is vastly different and beneficial”: but rather apply the old rules “so that the new rules remain untested and their (emphasis his) uncertain implications will continue to deter further consolidation”. Application of the new rules would, in effect, provide a proven blueprint for the Big 4 to use in future mergers….This is really an interesting take and may provide the reasoning behind the ¾ of the Big 4’s objections and has given me a reason to reflect in the “kick the can” thinking I had held previously.

- BTW, the old rules are not a pushover – I continue to believe the rejected SFSP deal is a model to look at, and the old rules led to the moratorium in 2001; in addition, as one example, it was the old rules that led to the conditions imposed on the UPSP (a merger based almost entirely on economies) that brought BNSF into such huge prominence in Texas.

Also:

- Here’s a link to the podcast I did on Friday with the irrepressible Jeff Berman of “Logistics Management” magazine: Railroad and Intermodal Markets Analysis and Review of Canadian Pacific-Kansas City Southern Deal - Logistics Management (CLICK HERE).

- My Ag-expert doubts that the deal will create many diversions of CP grain from Vancouver to the gulf because “Center Gulf/Texas Gulf are residual destinations because the drawing arcs pull the grain elsewhere” and forcing it there would be an “unnatural act”; meanwhile, why would CP not want to push grain to Vancouver?

Anthony B. Hatch

abh consulting

http://www.abhatchconsulting.com

abh18@mindspring.com

Twitter @ABHatch18