Everyone is cognizant that the supply chain disruptions and delays that ensued after COVID-19 were unprecedented. Logisticians, shippers, and importers, to name a few involved in global trade, faced more than two plus years of challenges with overwhelmed infrastructures, unpredictable increased demand, supply/equipment shortages, historic transportation/freight costs, and general supply chain volatility/bottlenecks never before seen at the scale we all experienced it.

While there were challenges, it should not be forgotten that many companies saw record revenues and EBITDA during this time period. Business was very good for many. The challenge was acclimatizing to that time period in business. Product decisions, associated costs of doing business, sell prices to customers, processes, and basic decision-making on the sourcing, manufacturing, order fulfillment, and shipment of goods had to be rethought sometimes even from scratch in board rooms across the world.

Now as the world continues to normalize on the path the world was on before the pandemic, transportation prices have come crashing down to reality. The economy has set in with challenges including inflation, reduced demand for products, and high inventories across supply chains; a striking reminder of the buying/ordering behavior of the last two years.

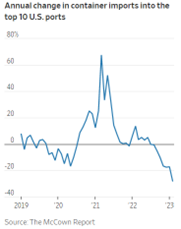

Shipping metrics are showing signs of weakening demand as companies continue to hold back new orders amidst high inventories and weakened consumer demand. Container imports at the ports of Los Angeles and Long Beach, the USA’s top port complex, dropped 38% year over year in February.