THIS IS NOT good news.

Industrial production, manufacturing, and general cargo trade lethargy continue through the first quarter.

Still no overall GDP recession metrics for the US economy.

But freight continues in “a funk” like pattern.

Not likely to get better by the Monday morning REF20 kick-off session on March 2nd.

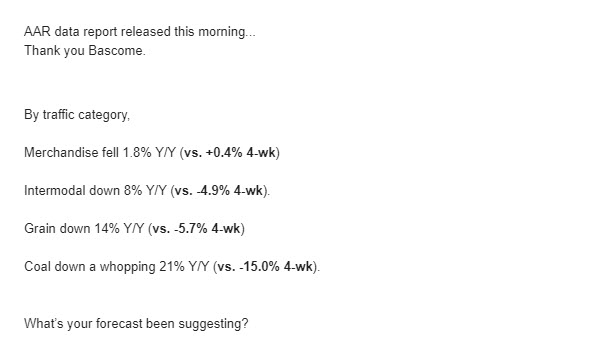

A different look geographically.

Week 7

- BNSF carloads were down 5.5% (vs. -1.9% 4-wk),

- UNP carloads fell 10.1% (vs. -8.5% 4-wk)

- CSX carloads down 5.6% VERSUS marginal +0.6% up in 4-wks trend

- NSC Carloads down 11.7%. Versus -7.6% 4-wks trend

- KCS traffic is up 7.3% Versus 4-wks +10.3% trend

- Canadian: CP RTMs rose 22.1% (vs. +12.1% 4-wk), but CNI RTMs were down 8.0% (vs. +5.1% 4-wk) as pipeline protests created blockades in their network.

BE MINDFUL PLEASE of this second way of interpreting rail freight into this year’s first quarter.

— Bascome’s group description is a bit more balanced...

‘Looking back at 15 years of U.S. rail volume data from the start of prior year 4Qs to the current 1Q-TD, total carloadings (carloads + intermodal) have tracked relatively in line with historic seasonality during early 2020.”

“Breaking it down in broad, end-market strokes, commodity and industrial-levered traffic have performed toward the upper end of historic trends, aided by strength in crude by rail and metallic ores and metals, along with some more recent strength in agricultural products.”

“This strength has been partially offset by softness in coal, which was largely expected in exports due to weak pricing and macro headwinds, though could see an incremental leg down in domestic utility as mild winter weather drove natgas below $2.00 for the first time since 2016.”

“On the consumer side, carloads have tracked relatively inline through early 2020 with recent weeks seeing strength in intermodal (driven by Chinese New Year pull forward) and automotive shipments.”

Bascome’s group asks —

“Where do we go from here?

— While the more cyclical businesses (i.e., industrial ex-coal & consumer) have seen seasonally inline performance to start 2020, we will continue to keep a close eye on these sequential trends as impacts from China's Coronavirus wouldn't hit U.S. rail supply chains until the end of 1Q and into early 2Q, with shipments out of China expected to be put on hold longer than is typical during the CNY holiday as factories slowly ramp up production following extended closures.”

Cheers!